How much do you need to retire and how can your Investment Policy Statement help you get there?

Jan 18, 2021When do you think you really need to start thinking about retirement? And what do you make of statements that say you need 3 or 5 million dollars to retire?

CHECK OUT MY FREE FINANCIAL INDEPENDENCE CALCULATOR HERE

When I got my first paycheck as an attending, I thought I would be all set to FIRE (Financially Independent Retire Early) in 2020… When I looked at my Financial Independence numbers in early 2019, I wasn’t close … and that’s not because I had not earned or saved as much as I expected to. It’s because

- I did not know exactly how much I needed saved up for retirement to be able to live off of it for the next 30-50 years…

- I did not realize how important it was to identify and be specific about my investment vehicles (ie asset allocation) during my years of saving and later in retirement because their rate of return would determine how fast my nest egg would grow and later how much I could safely withdraw without depleting it …

- In short, I did not have an Investment Policy Statement (IPS)

As simple as this may seem, knowing exactly what your goals are and having a plan to get there are the first and most important steps in your journey to financial freedom. So I ended up :

- with a much lower rate of return because of disproportionately large fixed income assets.

- buying liabilities instead of assets (luxury cars, large personal home etc) per Robert Kiyosaki’s definition where assets put money in your pocket and liabilities take money out of your pocket.

- and although I was fully contributing to tax advantaged accounts, in some ways I feel I was saving, not investing for retirement.

Fortunately I was able to make huge shifts in mindset and asset allocation in 2020 - I set intentional three year goals. Once I got started - I was able to hit my Financial Independence numbers in early 2021 - in under a year. I hope this post inspires you to make small shifts and look at Financial Freedom differently.

So how big does your nest egg need to be for retirement?? 1 million dollars? 2.5 million dollars?

It depends… (no cliched answers here, just mathematical ones…)

CHECK OUT MY FREE FINANCIAL INDEPENDENCE CALCULATOR HERE

- First calculate how much you need annually during retirement : Make sure you include your home mortgage (unless you will have paid it down in full by retirement), property taxes, cost of health care in retirement, home and car insurance costs, cost of utilities, credit card bills and everyday expenses, transportation costs (leasing or owning a car), vacations etc… Remember to factor in pension and Social security income;

- Annual need in retirement – (Social Security and pension) = Annual withdrawal from nest egg.

- Then decide which investment vehicles you will have in your nest egg… because the rate of return of your investments will determine how much you can withdraw safely every year without depleting your retirement egg. Factor in about 3% inflation rate for Stock/Fixed income assets, Income from rental real estate is inflation controlled.

- And finally have a goal for When you intend to retire. The earlier you seek financial freedom, the larger your contributions (accelerated acquisitions in case of real estate investments) to your nest egg will need to be every year. I am including a calculator that helps you calculate how much you need to save each month to hit your retirement goals here.. and your asset allocation and/or withdrawal rate will need minor modifications for stock/bond portfolios if u plan on retiring early.

Most people have a pure Stock/Bond portfolio that they hope to fund retirement with and there are numerous studies and recommendations for what your asset allocation should be for optimal rate of return and what withdrawal rates need to be to draw down your assets and have it last 30 years or more (it is very hard to live off the income from a Stock/Bond portfolio unless the portfolio is immensely large).

Some people use only Real estate investments to fund retirement, and the best part is – you can live off the income/ cash flow… and pass your assets down to your kids with a stepped up basis !! Win-win.

I use a hybrid Stock/ Bond/ Real estate portfolio which I will also discuss briefly. I want to point out that I will not be including commodities, cryptocurrency in this discussion as I feel for most people they don’t have a place in retirement planning and draw down strategies.

Pure Stock/Bond portfolio:

$ needed annually in retirement x 25 = Retirement Nest egg

For a pure Stock/ Bond portfolio to last you at least 30 years

So suppose you need your Stock / Bond portfolio to provide you with 60k annually in retirement, your nest egg should be 1.5 million dollars (60,000 x 25) and to safely withdraw 100k annually in retirement, your nest egg should be around 2.5 million dollars.

Now this may seem like a really large nest egg, but if you contribute 2000$/month or 24,000$ annually into an investment account that has an average 10% annual return, in 20 years you will be sitting on 1.5 million dollars. That is only 5000$ above the max limits for a 401(k) contribution at work. Or another way of looking at it is contributing the maximum into your 401k and Roth IRA (or back door Roth IRA for high income earners) for 20 years… Now this does not factor in long term capital gains taxes on your 401 (k) gains but draw down strategies are complex and best left for another post.

These numbers will work if :

- Weighting of Stock:bond portfolio at retirement is between 50:50 and 60:40. With historical Stock returns being around 10% and Bonds yielding around 5%, this portfolio should yield anywhere from 7.5% to 8%; factoring in 3% for inflation, that leaves you with a Safe annual withdrawal rate of around 4% to have the portfolio last at least 30 years (average rate of return – inflation) as shown by Bengen in 1994 (he revised safe withdrawal rate to 5% in 2020). [ 0.04 (withdrawal rate) x 1,500,000$ (nest egg) = 60,000$ (annual withdrawal)]

- Your Stock/ Bond portfolio investment returns match historical returns. I believe that the best retirement stock portfolios are predominantly composed of passive index funds (and not individual stocks) such as those offered by Vanguard (preferred for their passive management, low costs, wide diversification and tax efficiency).

- A popular strategy for Stock/Bond asset allocation is the 3-fund portfolio, which includes in varying proportions (based on your need for diversification, risk appetite and time to retirement) of

- Total US Stock Market Index Fund (VTSAX)

- Total International Stock Market Index Fund (VTIAX)

- Total US Bond Market Fund(VBTLX)

- Or if you are like me and prefer lesser portfolio volatility to small cap and international exposure, you can stick to a 2 Fund portfolio comprised of VFIAX (S&P 500 Index fund) and VBTLX (Total US Bond Market Fund).

- A popular strategy for Stock/Bond asset allocation is the 3-fund portfolio, which includes in varying proportions (based on your need for diversification, risk appetite and time to retirement) of

If you plan on retiring early, your portfolio needs to last longer which can be achieved by increasing your stock:bond allocation to 70:30 (these portfolios will however decline more sharply during big bear markets) or by decreasing the withdrawal rate to 3% (which is the safer option hopefully causing your portfolio to last 50 years or longer).

Stick to your plan for asset allocation through market ups and downs by periodically re balancing your portfolio. Over long periods the market will go up despite short term volatility and the withdrawal rate calculations only work if you stick to the plan at all times.

Want to plug your portfolio numbers in to CALCULATOR? Click here!

Pure Real estate portfolio:

Real estate Investing can be passive (REITs, syndication) or active (Joint Ventures or direct ownership). I prefer direct ownership for more control over the asset and higher rewards including increased tax benefits. I discussed FIRE with real estate in a previous post including how your rental real estate returns are actually much higher than just Cash on Cash (CoC) returns, but lets move ahead with the conservative approach of only including CoC returns in our calculations.

$ needed annually in retirement x 10 = Amount invested in rental real estate at time of retirement

For a pure Real estate portfolio (leveraged) to last you for ever

So suppose you need your Real estate portfolio to provide you will 60k annually in retirement, then you can reach this goal with around 600k of leveraged investments (60,000$ x 10= 600,000$) and so on. You could also calculate your annual cash flow from each door and see how many doors you need to own before you hit your and cash flow numbers for retirement.

These numbers will work if:

- you have 10% Cash on Cash CoC return from your real estate investments (post tax return for passive real estate investments).

- your investments are leveraged, meaning you have a mortgage on the property, which increases your rate of return. For example, if you buy one house for 200,000$ down and generate cash flow of 1000$ per month, your Cash on Cash return is 6%. But if you use the same 200,000$ and split it into 25% down payments for 4 homes each 200,000$ with mortgages on them and each generates 500$ in cash flow, your monthly cash flow is 2000$ or 12% CoC return.

Don’t forget the additional perks of real estate investing –

- Annual cash flow is tax free for most direct ownership in rental real estate due to depreciation.

- As your property appreciates in value and your renter pays down debt, your equity in the property is increases; you can tap into this equity by doing a cash out refinance without having to sell the property.

- Rent is inflation controlled

- In this scenario, unlike with a stock:bond portfolio, you are not drawing down assets – you are actually living off the income.

Now, if you factor in annualized return on investment for a simple buy and hold Long Term Rental property - this is typically over 20% (factoring in Cash flow and equity build up from debt pay down and market appreciation) - without using any advanced strategies for optimizing returns. You can tap into equity build up over time without paying taxes in many ways - cash out refinances, 1031 exchanges... Once this conservative estimate is factored into the equation :

$ needed annually in retirement x 5 = Amount invested in rental real estate at time of retirement

For a pure Real estate portfolio (leveraged) to last you for ever

Suddenly, the amount of money you need invested to hit your Financial Independence numbers has shrunk considerably - allowing you to FIRE that much faster.

Hybrid Stock:Bond:Real estate portfolio:

Some of you, like me, likely fall in this category and would rather not put all our eggs in one basket or like me are reluctant Hybrid investors.

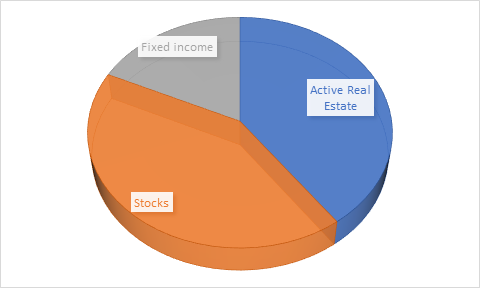

In my case, my FI number was slightly above 100k annual withdrawal in retirement. In mid 2021 this is what my portfolio looks like :

- 900k in stocks/bonds giving me a safe withdrawal of around 36 k annually

- 550 k in leveraged real estate investments (direct ownership) that invested at my average 15% COC yields 82k in tax free cash flow annually

That's close to 10k in passive monthly income !!

Now I like to be very conservative in my estimates -

- I have only included Cash flow from the rental properties in my analysis - not annualized ROI which is closer to 40-75% once you factor in equity build up and (variable) tax savings.

- I have also not included any active income from sporadic clinical assignments I may take up or income from GenerationalwealthMD and my Real Estate Coaching program in this calculation.

You will notice that adding real estate into the picture will propel you towards your retirement goals much faster. But again, it is very important to be specific about how many doors/ units you will need and your markets (I prefer cash flowing markets over markets that see higher property appreciation).

And that’s the end of a long post… Hopefully you already have a written Investment Policy Statement IPS that clearly states when you want to retire, how much you will need to retire and how you will be invested going forward to get to those goals . If not, there is no better time than now to get started!

CHECK OUT WHERE YOU STAND TODAY - FREE FINANCIAL INDEPENDENCE CALCULATOR

Looking for Resources to help you Start or Scale your Real estate portfolio so you can hit Financial Independence faster?

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.